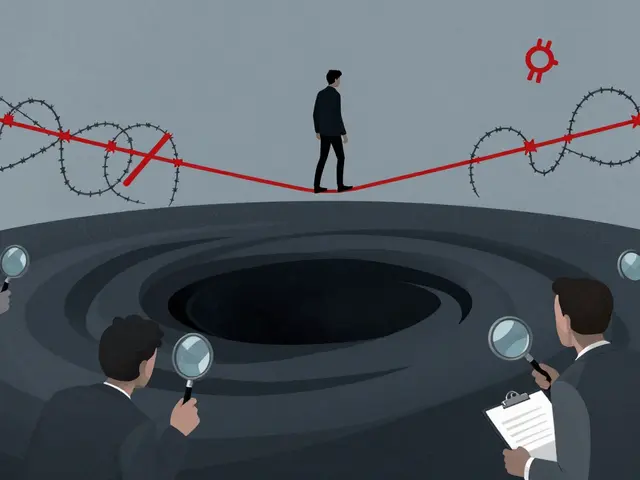

Withdrawing cryptocurrency to fiat in Russia feels less like a standard banking transaction and more like navigating a minefield. If you have tried to convert your Bitcoin or Tether into rubles recently, you likely noticed the friction. Your card might get blocked, your daily limit slashed, or worse, your account frozen for days while compliance teams dig through your history. This is not paranoia; it is the result of a strict regulatory framework that has tightened significantly since late 2025.

The core issue is simple: Russian banks are under immense pressure from the Central Bank of Russia (CBR) is the national central bank responsible for monetary policy and financial stability to stop unregulated money flows. With sanctions isolating traditional banking channels, crypto became a loophole for capital flight. The government’s response? They didn’t close the loophole entirely-they put tripwires everywhere. Understanding how these tripwires work is the only way to keep your funds accessible.

The New Reality: Federal Law No. 3-1092818-2025

To understand why your withdrawal got flagged, you need to look at the law that changed the game. Effective September 1, 2025, Federal Law No. 3-1092818-2025 grants Russian banks authority to immediately limit daily cash withdrawals to 50,000 rubles for 48 hours when transactions are flagged as potentially suspicious. This was a strategic escalation in a seven-year campaign against unregulated crypto circulation.

Before this law, banks had discretion. Now, they have mandates. The CBR reported that by the deadline, 98% of Russia’s 347 licensed banks had implemented the required monitoring systems. This means almost every major player-from Sberbank is Russia's largest commercial bank and state-owned financial institution to smaller regional lenders-is running automated scripts to catch crypto-related activity. If you trigger an alert, the system reacts instantly. You don’t get a call first. You get an SMS notification within 15 minutes telling you your daily limit is now 50,000 rubles ($600 USD) for the next two days.

This isn’t just about large sums. The goal is to disrupt the flow. Finance Minister Anton Siluanov confirmed in October 2025 that crypto accounts facilitated 37.2% of all cross-border currency withdrawals. The government wants that number down, even if it means making life difficult for legitimate traders.

12 Red Flags That Trigger Instant Restrictions

You might think you’re being careful, but the algorithms are looking for patterns humans miss. According to CBR Directive No. 74-P issued in August 2025, banks must monitor 12 specific transaction characteristics. Here is what triggers them:

- Unusual Timing: Withdrawals between 11:00 PM and 5:00 AM local time are viewed with suspicion. Why are you moving money at 3 AM?

- Odd Amounts: Transactions for amounts not divisible by 1,000 rubles raise eyebrows. Round numbers look like business; random digits look like laundering.

- Geographic Mismatches: Using an ATM more than 50 kilometers from your registered address is a major red flag.

- Digital Tools: Using QR codes or virtual cards instead of physical payment instruments often triggers deeper scrutiny.

- Phone Activity: Yes, really. Sudden changes in phone activity, such as receiving three or more messages from unknown numbers within six hours before a withdrawal, can flag your device as compromised or involved in a scam.

- Rapid Cash-Outs: Withdrawing cash within 24 hours of receiving a transfer exceeding 200,000 rubles via the Faster Payments System is automatically monitored.

- Device Health: Signs of malware infection on your phone or computer linked to the banking app will halt transactions.

- P2P Platform Links: Transactions linked to platforms like LocalBitcoins or Paxful exceeding 100,000 rubles are high-risk categories requiring automatic flagging.

If you hit any of these, the 50,000 ruble limit kicks in. But the real headache starts after the 48-hour window expires. That’s when the human compliance team gets involved.

The Compliance Gauntlet: What Happens After the Freeze

Once the automated system flags you, the ball moves to the bank’s anti-money laundering (AML) department. In mid-2025, these departments were small. Today, they are massive. Sberbank alone hired 217 specialized analysts by September 2025. VTB and other major banks expanded their crypto monitoring teams by 300-400%.

When your account is under review, expect delays. Average resolution times for flagged conversions dropped from 2.3 hours to 18.7 hours. For complex cases, it takes days. On forums like BitBoom and Reddit’s r/RussianCrypto, users report average resolution times of 3.2 business days. During this time, your money is stuck.

What do they ask for? It’s not just ID anymore. Banks increasingly demand notarized transaction histories from exchanges. If you use decentralized platforms (DEXs) that don’t maintain records, you are in trouble. You may be asked to prove the source of funds, provide contracts for goods purchased, or explain why you received money from a stranger on a P2P platform.

| Action Triggered | Immediate Consequence | Duration | Resolution Requirement |

|---|---|---|---|

| Minor Flag (e.g., odd amount) | Daily limit reduced to 50,000 RUB | 48 Hours | None (auto-lifts) |

| Major Flag (e.g., P2P > 100k RUB) | Account Frozen / Blocked | 3-7 Days+ | In-person verification + Source of Funds proof |

| Repeated Violations | Account Closure | Permanent | N/A (Blacklisted) |

Why P2P Trading Is the Most Dangerous Zone

Peer-to-peer (P2P) trading used to be the lifeline for Russians wanting to move crypto to fiat. In Q2 2025, it accounted for $2.1 billion in monthly volume. Now, it is the primary target. The CBR’s internal document 'Recommended Indicators for Cryptocurrency-Related Suspicious Activity' explicitly names P2P platforms as high-risk.

Here is the problem: When you sell USDT on a P2P platform, the buyer sends rubles to your card. To the bank, this looks like a random person sending you money. If you then withdraw that cash, the bank sees: Random Person → You → Cash Out. That is the textbook definition of money laundering.

Anton Klyachyn, founder of Chainalysis Russia, warned in September 2025 that these restrictions create artificial friction points that benefit criminal intermediaries. These "cleaners" charge 7-12% premiums to bypass restrictions by using mule accounts. But for the average user, engaging with these services is illegal and risky. The legislation progressing through the Duma introduces criminal penalties for repeated violations, with potential sentences up to 5 years for "organized cryptocurrency conversion schemes."

Strategies for Navigating the New Landscape

If you must trade crypto in Russia, you need to adapt. Legal expert Alexey Likhunov recommends treating your banking relationship like a long-term project, not a utility. Here are practical steps based on current data:

- Build a "Natural" History: Use cards with at least 3 months of regular spending patterns. Groceries, utilities, subscriptions. This shows the bank you are a normal consumer, not just a crypto trader.

- Limit Conversion Frequency: Don’t cash out every day. Space out transactions. High frequency triggers algorithms faster than high volume.

- Stick to Known Counterparties: Transactions with verified contacts face 73% lower restriction rates. Avoid anonymous P2P sellers whenever possible.

- Use Multiple Accounts Carefully: Many traders use 3-7 accounts to stagger withdrawals. However, AML algorithms now monitor cross-institutional activity. If you move money between your own accounts too frequently, you trigger a different set of alerts.

- Avoid Late-Night Transactions: Keep all banking activities between 9 AM and 9 PM. It sounds trivial, but the algorithm penalizes 3 AM withdrawals heavily.

Remember, the goal of the CBR is not to ban crypto entirely-it is to control it. The dual-track approach allows institutional banks to handle crypto for foreign trade (capped at 1% of regulatory capital) while crushing domestic retail circulation. As a retail user, you are in the latter category.

The Future: Criminal Penalties and Digital Ruble

The situation is not stabilizing; it is tightening. By December 1, 2025, new rules require banks to verify sources for any withdrawal over 100,000 rubles. Meanwhile, the digital ruble is scheduled for phased rollout starting September 2026. This central bank digital currency (CBDC) will offer a controlled alternative to decentralized crypto.

The IMF warned in October 2025 that this fragmented regulation creates systemic vulnerabilities. But for you, the individual trader, the message is clear: The era of easy, anonymous crypto-to-fiat conversion in Russia is over. Every ruble you withdraw is watched. Play by the rules, keep your history clean, and assume that any large movement of funds will require explanation.

Can I still withdraw crypto to my Russian bank card?

Yes, but with significant restrictions. Under Federal Law No. 3-1092818-2025, banks can immediately limit your daily withdrawal to 50,000 rubles for 48 hours if a transaction is flagged as suspicious. Larger amounts may require in-person verification and proof of income source.

Which banks are most restrictive towards crypto users?

All 347 licensed banks in Russia have implemented CBR monitoring systems. However, major players like Sberbank and VTB have expanded their compliance teams significantly, leading to longer processing times (averaging 18.7 hours for flagged transactions). Smaller banks may be slower to react but are equally bound by the law.

Is P2P trading illegal in Russia?

P2P trading itself is not explicitly banned, but it is heavily scrutinized. The CBR identifies P2P transactions exceeding 100,000 rubles as high-risk. Repeated violations of withdrawal restrictions related to P2P activity can lead to criminal charges under new legislation proposing up to 5 years imprisonment for organized conversion schemes.

How long does it take to unfreeze a crypto-flagged account?

For minor flags, the 50,000 ruble limit lifts automatically after 48 hours. For full freezes requiring documentation, the average resolution time is 3.2 business days. Complex cases involving large sums or unclear sources of funds can take weeks and require visiting a branch in person.

Will the digital ruble replace crypto?

The Central Bank aims to reduce unregulated crypto circulation by 85% by 2027. The digital ruble, launching in phases from September 2026, is designed to be the official channel for digital payments. While it won't replace private crypto holdings, it offers a regulated alternative for domestic transactions without the risk of bank blocks.

Mauricio Contreras Loredo

June 11, 2026 AT 08:27Oh wow, another country turning banking into a dystopian nightmare. Just wait until they start fining you for breathing too loudly near an ATM.

Kenneth Riley

June 12, 2026 AT 00:53Let's be real here this isn't about security it is about control and the sheer incompetence of the CBR to manage actual financial flows so they just break everything instead of fixing it

you think round numbers are suspicious? please. the algorithm is basically screaming 'I am stupid' while freezing accounts that have been active for years. i watched my friend get blocked for buying groceries at 4am because he had insomnia. the system is broken beyond repair and anyone thinking they can outsmart a bureaucratic monster is delusional

Grace Newman

June 12, 2026 AT 12:04It is imperative to note that these measures are not merely regulatory but part of a broader surveillance state apparatus designed to eliminate any form of unmonitored economic activity.

The correlation between the implementation of Federal Law No. 3-1092818-2025 and the subsequent rollout of the digital ruble suggests a premeditated strategy to centralize all financial power under the direct oversight of the Central Bank. One must consider that the 'suspicious activity' flags are likely calibrated to target specific demographic groups or political dissidents who utilize crypto for legitimate privacy reasons. The mention of 'malware infection' as a trigger is particularly sinister, implying that the state may actively inject code into devices to justify freezing assets. We are witnessing the erosion of financial sovereignty in real-time, and those who remain silent are complicit in their own subjugation.

Kumaran sowkarpet

June 14, 2026 AT 09:27hey guys just wanted to say this is super scary :(

i heard from some friends in moscow that even using qr codes gets you flagged now?? that is crazy right :O

hope everyone stays safe out there

ravi mahla

June 15, 2026 AT 10:17Haha, classic Russian bureaucracy. They probably flag you if you blink at your phone too fast. Enjoy the 50k limit, comrades!

Benjamin Eisen

June 16, 2026 AT 04:08I mean its kinda wild how strict it is but i guess with sanctions flying around they gotta do something right?

just dont do anything sus like withdrawing cash at 3am lol

also try to keep your history clean maybe use diff cards for grocery shopping vs crypto stuff

hope that helps someone out there navigating this mess

Mark Brunschwiler

June 16, 2026 AT 05:39money is just a story we tell ourselves and when the government decides to change the story you become the villain for reading the old pages

it is sad really

people used to trust banks now they trust nothing except cold hard cash which also disappears

we are all just ghosts in the machine waiting to be deleted by an algorithm that does not understand human pain or desperation

why do we struggle so much for freedom when the cage is made of our own fears?

Abby Sivertsen

June 18, 2026 AT 02:28This is honestly terrifying. I can't imagine living with that level of scrutiny on every single transaction. It feels like they're punishing people for trying to survive economically. The part about P2P being the 'most dangerous zone' makes me want to cry. People just need to move money safely and they're treated like criminals. It's such a hostile environment for regular folks.

sreeja boora

June 19, 2026 AT 09:42It is quite evident that the Indian financial sector operates with far greater transparency and logical consistency compared to the chaotic regulatory framework described herein. While Russia struggles with arbitrary freezes and opaque algorithms, our systems prioritize stability and clear compliance pathways. This situation highlights the necessity of robust, predictable legal structures rather than reactive, punitive measures that hinder legitimate commerce. Citizens deserve a banking environment that supports growth, not one that instills fear through random restrictions.

Suman Patil

June 21, 2026 AT 00:33Look, we all know the geopolitical landscape is messy right now, but let's try to find common ground here. Whether you're in Mumbai, Moscow, or New York, the frustration with over-regulation is universal. The key is to stay informed and adapt without losing hope. Let's support each other by sharing tips on how to navigate these complex systems legally and safely. We are stronger when we share knowledge rather than succumbing to fear. Keep calm, stay compliant, and remember that community support is vital during these challenging times.